As an investment management start-up we constantly get asked the question – How does investment in commercial real estate compare to other investment avenues?

In this blog, I am going to address that question by analyzing returns from various investment options.

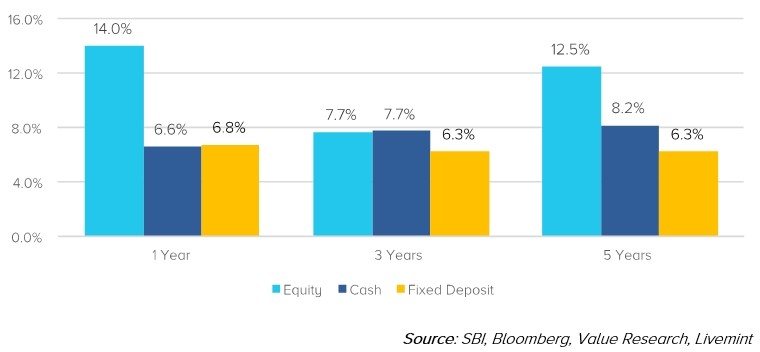

Let’s start by looking at how Equity (Stock Market), Fixed deposits and Cash (money market funds) have performed over 1, 3 and 5 years horizons.

Chart 1: Returns from Equity, Cash and Fixed Deposits

Equity has been the clear winner, as it should, given the higher risk associated with this investment. Investors in equity were compensated by almost double the returns of the fixed deposits. This is significant given that inflation averaged above 5-6% during this period rendering real returns from fixed deposits close to zero. This chart highlights an important factor in investing - the risk-return matrix. Let’s take a look at this matrix more closely with the help of two extreme and very popular products available to the retail investor today - Fixed Deposits and the Stock Market (Equity).

Chart 2: Risk Return Matrix

Fixed Deposits

Fixed deposits have the lowest return and the lowest risk and the Stock market has the highest return and the highest risk. While investing in an FD, your principal will always be safe (in most cases) but in the stock market you could lose half your capital in a day. To compensate for lower risk, the returns are obviously lower in an FD. The current FD rates of all banks are given in the chart below:

Chart 3: Fixed Deposit Rates

Debt Funds

To get higher returns than FDs, an investor can also look at debt mutual funds. These funds invest in a mix of government bonds (issued by the government of India) and corporate bonds (issued by various AAA, AA rated corporates). Depending on the mix of securities, the returns can vary between 9-11%. However, there is no upside potential in this product. Getting 18-20% returns are close to impossible here. Below are some of the highest performing debt funds in the market today.

Chart 4: Returns from Top 10 Debt Funds

Commercial Property

So where does property investing fit into this matrix? Property and in particular commercial property has a unique characteristic. In a way, it is a hybrid between fixed deposits/debt mutual funds and equity but with a lower downside risk and a higher upside possibility. Commercial property investors get the monthly rental yield of 7-8%, which increase every year, plus a share of the capital appreciation of the property.

If chosen correctly, a smart asset manager can significantly lower the downside risk while keeping the upside potential intact. This according to me is where the Asset and the Asset Manager distinguishes itself.

Commercial property investment can return anywhere between 15-25% per year with 8% as the lower threshold thanks to the rental yield. Further two important factors make it a much better investment option compared to FDs – The annual rent escalation protects your investment from inflation and the lower tax regime protects your post tax returns.

While an individual pays 33% tax on FD interest, rent is only taxed at 21%. If the FD/Post office schemes give a bonus that too is taxed at 33% whereas capital gains from commercial property are taxed at only 20% (lower after accounting for indexation). For understanding more about how tax works be sure to check our blog on Taxes in Property.

Unfortunately, this product is not available to the retail investor today. Due to the high cheque sizes, this product has so far been the preserve of HNIs leaving retail investors the option of buying smaller and lower quality properties. However, technology is changing this and at Property Share we are making this happen by allowing normal retail investors to participate in this product at much lower investment sizes.