As I write this, the novel Coronavirus has infected over 380,000 people with the death toll at close to 17,000. As the CEO and Co-founder of a real estate investment platform, I often get asked the question - How does this affect real estate investing?

As most of the world goes into lockdown, we see the impact of the pandemic in the following ways on real estate in descending order of impact:

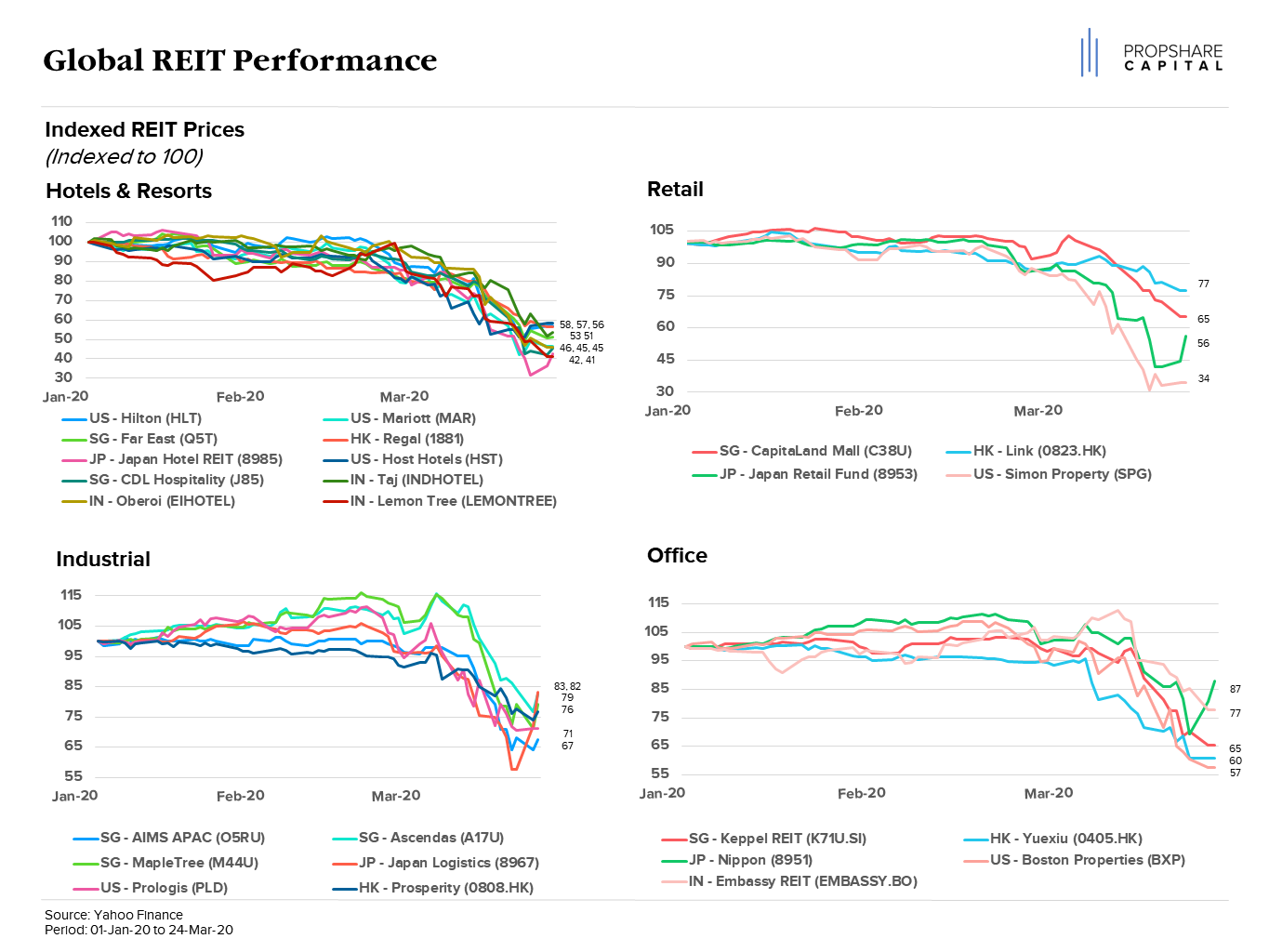

1. Hotels: The most affected asset class within real estate will be Hotels for obvious reasons. Hotel stocks around the world have seen significant fall in stock prices in anticipation of falling occupancies and room rates.

2. Retail Malls: Next in line are retail malls. Malls have been the first to be shutdown as governments try to limit large gatherings. Retailers will be hit hard and will negotiate rents during those months with landlords. Once normalcy returns, a few more weeks or months of lower rent might have to be extended to get them back on their feet.

3. Warehouses: Industrial activity has reduced significantly in the last 3 months. This has led to very low demand for logistics assets like warehouses. E-commerce companies are the only ones holding demand in the segment but that too is bound to slow down.

4. Office: The last asset class to be affected is Office. There are two types of tenants here - front office tenants and back offices tenants. Front office tenants, though not affected immediately will see an impact in the medium term as hiring freezes kick-in and a general recessionary mindset sets-in. This maybe countered by governments that provide quantitative easing and lower interest rates. The US federal reserve has slashed interest rates to 0.0%, the lowest since the 2008 financial crisis and added $1.5 trillion of liquidity in the banking system. Other countries are following suit.

Back-office tenants have proven to be quite recession proof as we saw in the 2008 crisis where office take-up and rents in cities like Bangalore, Pune and Hyderabad actually went up as multinationals outsourced more functions. These are also large leases and long term in nature. Hiring and employee churn has been a much bigger issue for tenants as rents tend to be a very small percentage of operating costs. With depreciation in the INR, rents in dollars terms have pretty much remained the same for these tenants over the last 10-15 years. Having said that, in the immediate term, large lease decisions will be delayed. If governments enforce lock down of offices, tenants may cite a force majeure clause and not pay rents during that time. However, this will have a very small impact on cash flows.

5. Leveraged Assets: If there is leverage in any of the above asset classes, the impact will be compounded. Leveraged hotel operators, malls, warehouses and offices will face markdowns as banks call loans and insist on higher security. With revenue and operational income going down, interest and principal payments will become a significant burden on underlying assets, however good the quality.

Positive Impact on Cap rates:

Cap rates are yields at which real estate assets are available in the market. In India, cap rates are currently 7-9%. Cap rates are directly correlated with the interest rates in the market. When interest rates go down on other investment products, cap rates on real estate go down as well. We expect interest rates to go down everywhere in the world as governments try to ease the burden on banks and financial institutions and resuscitate consumer demand. This will likely drive cap rates lower which can provide significant upside to real estate investors when it is time to sell the assets.

What Investors Should Do

1. Try signing leases with yearly escalations of 5% instead of 15% every 3 years so that tenants find the increase more gradual.

2. Try looking for leases which have longer lock-ins and where tenants have spent on the fitouts. This makes them sticky and Tenants tend to vacate these leases last.

3. Investors should look to purchase assets at below replacement cost (cost of buying land and building the property from the ground-up). This will mean that rents cannot go down much lower as new builds will take higher costs to be developed.

4. Use little or no leverage in buying assets that do not have long lock-ins so that you match the riskiness of rental cash flows with interest and principal payments.

5. Look for Grade A multinational tenants for whom rental costs are a small proportion of total revenues so that they do not look at these assets as cost centres.

6. Purchase only completed lease assets so that leasing and development risks are fully mitigated. The last thing you want to be doing in these situations is to look for a new tenant or be dealing with a rogue developer.

At PropShare we are conservative investors and have only invested in assets with long term leases and lock-ins and ZERO leverage. Almost all our tenants are back office tenants who have large set-ups with a long term commitment to India. We have insisted on purchasing assets where fitouts have been done by tenants in locations where vacancy is generally less than 5%, making them sticky and unlikely to vacate. All our assets have been purchased below replacement cost and have in-place rents that are below market. We recently negotiated a 15% escalation in our largest asset to 12.5% provided the tenant provides a further 3 year lock-in. These strategies pay the biggest dividends during these times of crises.

Remember that profit in real estate is made at the time of buying and not selling. Historically, returns have been highest when purchases have been made prudently at times of distress and fear. You should be looking at various opportunities which you had lost earlier by not giving-in to seller’s demand for high prices which you are expecting to come back cheaper now. Successful real estate investing is about identifying asset and pricing cycles and crystallising the right investment thesis at the right point in the cycle.